The shift to outcomes-based regulation presents challenges given the duty has a broad and wide-ranging impact across all aspects of business (e.g. firms will need to consider product suite, communications, end to end customer journey, changes to governance, product design and pricing in the context of demonstrating good value).

Key Challenges Include:

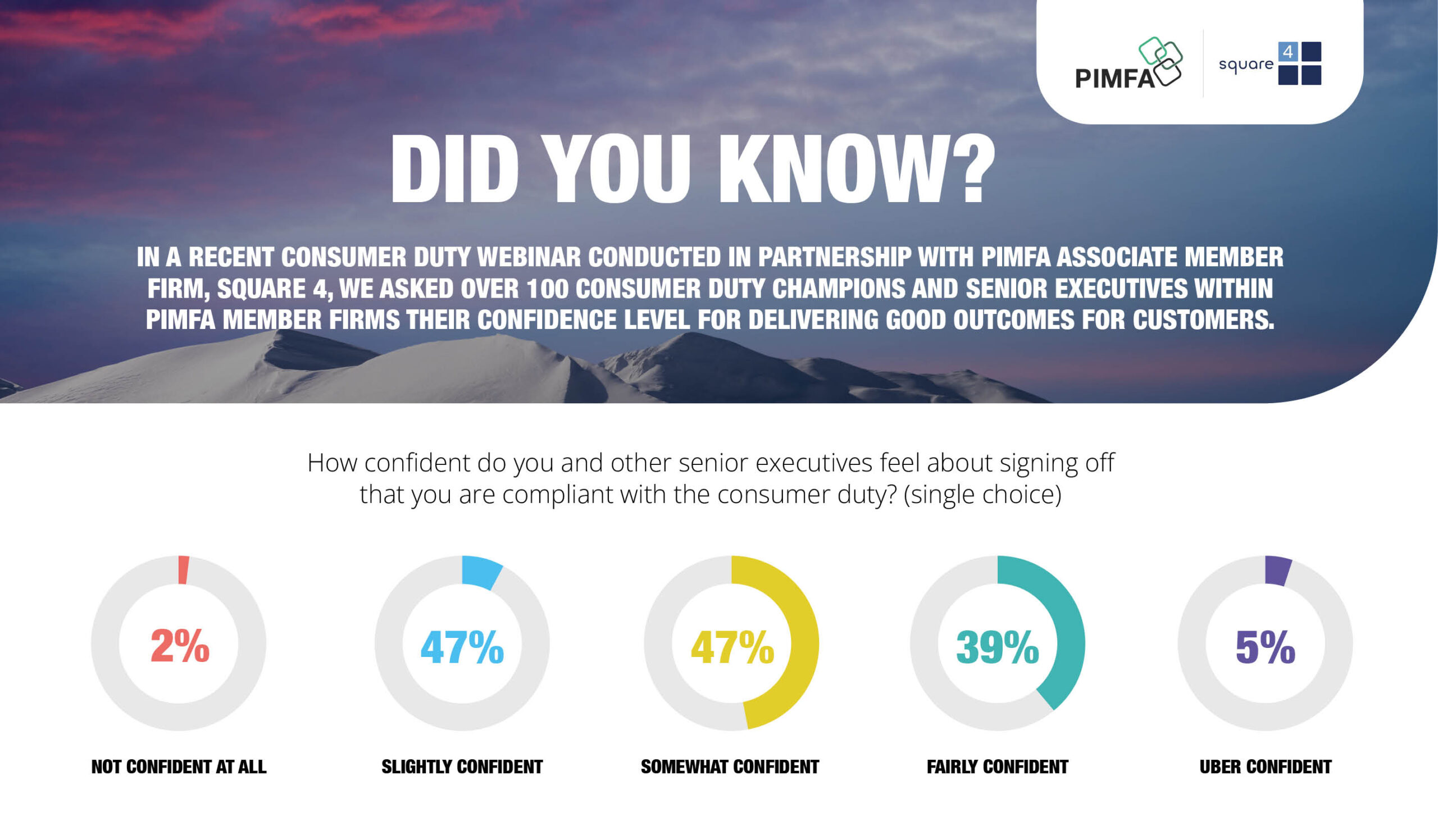

The introduction of Consumer Duty in July 2023 highlighted both the importance of evidencing compliance with data and MI and the expectation of financial services firms to have a consumer centric focus.

Culture is critical to compliance and the obligation to deliver good outcomes and fair value to all retail clients should be embedded throughout firm culture, policies and procedures to meet requirements under the four outcomes and cross cutting rules.

The ongoing monitoring and review of products, services and communications are expected to continually inform adaptations and improvements to facilitate the delivery of good outcomes whilst ensuring fair value for clients.

Consumer Principle 12

Consumer Principle 12: A firm must act to deliver good outcomes for retail consumers.

The Consumer Principle imposes a higher standard of conduct than existing Principles 6 and 7 – and sets a higher expectation of standards of conduct for firms (with an emphasis on consumer outcomes) and harmonises rules across the financial services industry to enable good outcomes for retail customers. Compliance with regulatory obligations such as treating customers fairly, PROD and SM&CR provide a good foundation for firms in meeting requirements under the duty.

What ‘good’ looks like across the industry will be variable, dependent on clients’ specific circumstances and outcomes may be impacted by market conditions and/or global geopolitical factors. Given the subjective nature of the duty, it is incumbent upon firms to be able to evidence the steps taken to ensure good consumer outcomes in the event of this being challenged.

Cross Cutting Rules

Principle 12 is underpinned by cross cutting rules and four outcomes which aim to provide greater clarity to firms on the FCA’s expectations to drive a higher, consistent level of good outcomes across the industry.

A firm must:

Act in good faith toward retail customers

Avoid causing foreseeable harm to retail customers

Enable and support retail customers to pursue their financial objectives.

As compliance with existing rules may confer deemed compliance with some elements of the duty, firms can utilise existing compliance procedures as a foundation for meeting their obligations under the duty (e.g. advice firms may find they already comply with these rules under the current regulatory framework).

Firms must give consideration to the four outcomes (which set out detailed expectations of the firm-consumer relationship):

1. Products and services – products and services are fit for purpose, designed to meet consumers’ needs 2. Price and value – ensure the price of a product or service reflects fair value 3. Consumer understanding – ensure communications can be understood/help the customer make informed decisions 4. Consumer support – ensure the standard of customer service meet consumers’ needs and expectations

PIMFA

PIMFA